Boston Consulting Group (BCG) just published a great piece on potential agentic commerce futures. The report, "Agentic Scenarios Every Marketer Must Prepare For," starts off by admitting that no one knows what is going to happen in the space, but also that doing nothing at all is definitively the wrong move.

I came across it through Roger Dunn's breakdown in Edition 30 of his AI Commerce Brief (check it out here), which layers BCG's framework alongside Stripe's five levels of agentic commerce and McKinsey's automation curve work. If you haven't read Roger's piece, I'd recommend starting there for the full context across frameworks. He does a phenomenal job connecting the dots.

After reading both Roger's analysis and the original BCG report, I wanted to add in some of my thoughts, especially as they relate to merchants. Some points where I agree strongly, some where I think the framing falls short, and some where I think the conversation needs to go in a different direction entirely.

What BCG Got Right (IMO): Scenarios Over Forecasts

BCG's core argument is that most companies are asking the wrong questions. "When will agent-driven purchases hit critical mass?" "Which categories go first?" These are forecast questions, and forecasts require stable variables, or really any variables, and we don't have those.

Agentic commerce itself is a moving target. Consumer adoption is unpredictable. Regulatory frameworks are forming in real time across different geographies. And competitive responses from platforms, retailers, and brands are reshaping the field faster than any model can track.

The better question, and where BCG nails it, is... how do we build capabilities that work whether the market is 10% agent-driven or 90%?

BCG breaks the uncertainty into three layers... technology, human behavior, and market structure. All three are moving at the same time, which is exactly why forecasting doesn't work here.

I've been in the agentic commerce space long enough (9 months lol) to know that anyone who tells you they know exactly how this plays out is either selling you something or not paying close enough attention. And just to reiterate, the amount of people who said agentic commerce would never happen to begin with have mostly all gone quiet since OpenAI, Google, Stripe, Shopify, and Target have gotten involved.

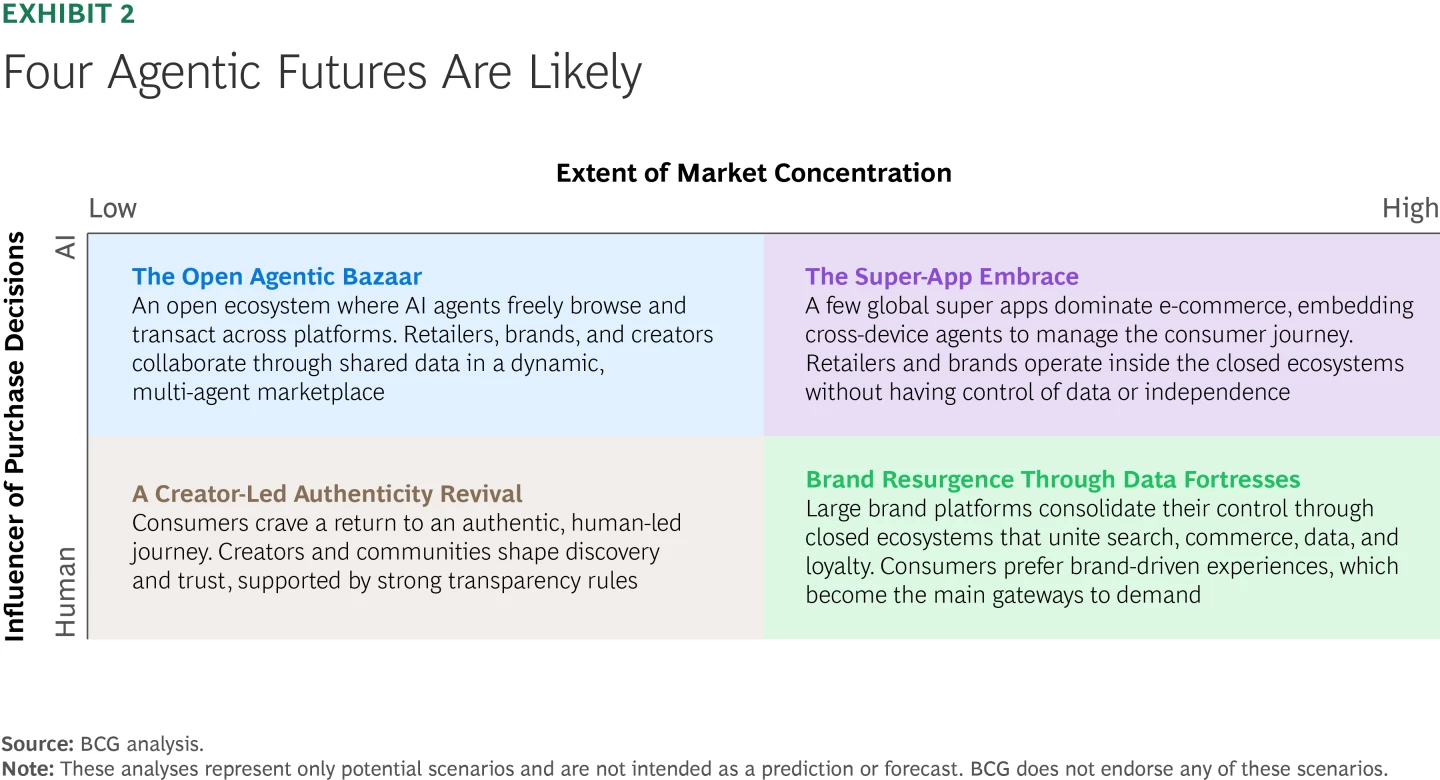

The Four Futures

The report identifies two variables that shape everything:

Variable one: Where does influence reside? With human judgment, social networks, and community trust? Or with algorithmic optimization, data signals, and machine-readable product attributes?

Variable two: How is market power distributed? Concentrated among a few dominant platforms? Or distributed across many competing agents in open ecosystems?

Cross these two dimensions and you get four worlds:

- The Open Agentic Bazaar - Distributed power, algorithmic influence. No single platform dominates. Agents roam freely across brands and retailers.

- Brand Resurgence Through Data Fortresses - Concentrated power, algorithmic influence. A few large platforms bundle search, commerce, data, loyalty, and proprietary agent engines into closed ecosystems.

- The Super-App Embrace - Concentrated power, human and algorithmic hybrid. Tech giants embed AI agents into daily life and own the customer relationship.

- Creator-Led Authenticity Revival - Distributed power, human influence. Trust flows through creators and communities, not algorithms.

Four Agentic Futures per BCG.

Roger added current examples for each of these in his breakdown... Google's UCP and OpenAI's ACP for the Bazaar, Amazon's Rufus and Walmart's Sparky for the Data Fortress, OpenAI's Instant Checkout for the Super-App, and TikTok Shop for the Creator Revival. I'd also add WeChat as the existing Super-App model, and YouTube Shopping and Substack communities on the Creator Revival side.

BCG recommends not picking one but preparing for all four. That's good advice. But I think several of these futures deserve a harder look.

On the "Open Agentic Bazaar"... Is It Actually Open?

This is the world many protocol enthusiasts are building for. Google's UCP, OpenAI's ACP, and the broader interoperability push all land here if they succeed.

But even in the Open Agentic Bazaar, it really isn't open. This isn't "open agentic commerce" if we are saying that participation sits on the rails of protocols that require merchants to build for. Which one is then the right one to build for to be open?

The Open Agentic Bazaar is really just merchants being merchants and operating as they are now, AND doing additional work to optimize their product data readiness to make sure that their content and context are aligned with how these LLMs and agents discover. That's not a new world. That's the current world with a data optimization layer on top.

On the "Data Fortress"... This Is Just E-Commerce Now

BCG describes this as a few large brand and retail platforms dominating, bundling search, commerce, data, loyalty, and proprietary agent engines into closed ecosystems. I'll give BCG credit for one distinction here... it's not just walled gardens, it's walled gardens with AI agents they control. That is an escalation from where we are today.

But the underlying dynamic is what e-commerce already is, minus the further development of those walled gardens. And I don't think it is a reality that is built for consumers. When brands are negotiating with gatekeepers who control both the agent and the data, brands are effectively being controlled by those walled gardens. BCG's own report acknowledges this risk directly.

We've already seen what this looks like in practice. When Amazon launched Buy for Me, merchants discovered their products had been listed without authorization, including out-of-stock items. The system generated unique email addresses per order, stripping merchants of customer relationships, loyalty program data, and any ability to cross-sell. Merchants didn't opt in... they had to contact Amazon to request removal. That's the Data Fortress in action, and it's exactly the dynamic that BCG is describing as a potential "future" that is already playing out today.

On the Lack of Nuance

One of my main takeaways from the BCG framework is that there still is a large amount of black or white even in these four agentic futures. As I have said before, there is oddly little nuance in the agentic commerce conversation.

BCG does acknowledge that AI adoption will be uneven across product categories, countries, and consumer segments. Roger builds on this point well in his piece, noting that your grocery shopping might live in the Data Fortress while your electronics purchases happen in the Bazaar and your fashion choices flow through the Creator Revival. I really appreciate that distinction.

But the four quadrants themselves are still too clean. BCG is adding two splashes of gray to sit in between a lot of black and white.

Where I Entirely Agree: Discoverability

The focus on discoverability is where I agree the most.

40% of Gen Z starts searches on Instagram or TikTok. ChatGPT ranked fifth in monthly website visitors in 2025, surpassing Amazon. Google's AI Overviews appeared in 21% of all searches. And BCG's own analysis found only 8% to 12% overlap between traditional search results and AI-generated answers.

That last stat is the most impactful... if your entire discoverability strategy is built around traditional SEO, you are missing somewhere between 88% and 92% of what AI answer engines are surfacing. That gap is massive, and it's only going to grow.

I believe there are phenomenal companies working in the discoverability space right now. If I were a brand, I would want to evaluate companies that have an interest in data behind their PDP optimization. What do before and after case studies look like? And how are they tracking what success and lift look like in discoverability as it relates to these answer engines?

Where I Disagree: "Machine-Readable Product Data Accessible via Standardized Protocols"

BCG says that in the Bazaar, discoverability means "machine-readable product data accessible via standardized protocols." I have a problem with this framing.

Which protocols are standardized? ACP? UCP? What about HTTP? Every merchant and user in the world already has adopted and trusts this protocol the most for their delivery of information. If that is the case, why should data need to be available for protocols that aren't already adopted and doing volume?

The web already works. Merchants already have websites. The infrastructure for delivering product information to anyone, human or agent, already exists. The real work isn't adopting a new protocol... IMO it's making sure your existing product data is rich enough, structured enough, and contextual enough for these LLMs and agents to actually understand what you're selling.

On Desirability: Right Concept, Wrong Sequence

BCG frames desirability as "the power to be wanted once you're found," and argues that strong brands with clear differentiation and verified quality signals have an advantage regardless of the scenario.

I'm not saying desirability doesn't matter... I'm saying discoverability comes first, and most brands haven't solved that yet. Agents as they are currently are still not that great at understanding intent, and optimizing for desirability seems to take the conversation a step further when optimizing for discoverability and machine-readiness might be a better priority right now.

Focus on discoverability first.

On Brand Equity: Completely Agree

76% of marketers say cutting brand spending has a greater negative impact today than five years ago. Trust correlates with an 8 percentage-point boost in BCG's "First Fast Response" metric. And as BCG puts it, "Even in an agentic world, branding won't matter less... it will matter differently, but even more than it used to."

Brand matters more, not less.

On Speed: Agree, But With a Caveat

BCG says moving to an AI-first marketing organization can triple marketing ROI, speed, and volume, translating to 5% to 10% incremental growth and 15% to 20% efficiency gains. They outline five capabilities to get there... embedding AI talent in marketing teams, continuous training, clear KPIs, integrated tooling, and governance guardrails.

I agree with all of this, but make sure you're value adding. There is a lot of conversation taking place right now regarding Google's spam changes to ensure that mass produced AI slop doesn't win. Speed without quality isn't a differentiator. BCG's five capabilities list actually supports this... it's not just "go faster," it's structured, governed investment in speed.

On BCG's Three Options for Brands: Missing the Obvious One

BCG gives brands three options. Build proprietary AI assistants on their own platforms. Meet consumers inside existing AI platforms through plugins and integrations. Or integrate with LLM platforms directly through protocols like ACP and UCP to reduce retailer dependence.

Roger makes a great point in his piece that this third path isn't retail dependence replaced by freedom... it's retail dependence replaced by platform dependence. I'd build on that even further.

What about meeting consumers where they already are... like on their own website? Why not optimize for agents on your actual website?

Also, what percentage of users and consumers are driving what amount of revenue to necessitate the technical lift required to get involved in these gated channels for the opportunity to potentially grab some of that volume?

I 100% agree on PDP optimization and increased content and context for agent readiness. But then why build for the individual protocols when you have zero clue which one will actually be most heavily adopted?

Optimize the digital real estate you already own. Make your product data richer and more machine-readable on your existing website. Ensure your content and context are aligned with how these agents discover. That work pays off no matter what.

Takeaways

I like BCG's conclusion that the price of indecision compounds faster than the cost of a mistake. Companies waiting for clarity on which agentic future will arrive are making the most expensive bet of all... a bet on the status quo.

But the action step is simpler than BCG's framework implies. Start testing. Start evaluating. Don't wait for OpenAI or Google or Target to lead the channel. Start with the digital real estate that you ALREADY own and have ALREADY built for.

The 8% to 12% overlap between traditional search and AI answers tells you everything you need to know about the urgency. Make sure that when any agent looks for what you sell, it can actually find you.

Sources

- BCG: Agentic Scenarios Every Marketer Must Prepare For

- Roger Dunn: Stop Predicting the Agentic Future, Start Preparing for Four of Them

*posted originally on LinkedIn - link*

Frequently Asked Questions

What are BCG's four agentic futures?

BCG maps two variables, where influence sits (human judgment versus algorithmic optimization) and how market power is distributed (concentrated versus distributed), into four worlds: the Open Agentic Bazaar, Brand Resurgence Through Data Fortresses, the Super-App Embrace, and a Creator-Led Authenticity Revival. BCG's advice is to prepare for all four rather than bet on one.

Should brands optimize their existing website or build for new protocols like ACP and UCP?

The web already works and merchants already have websites. Rather than betting on which protocol gets adopted, the work that pays off regardless is making your product data richer and more machine-readable on the site you already have, and aligning your content with how agents discover.